Repossession is what happens when a creditor takes property put up as collateral because you’ve defaulted on the debt. Strict rules control what a creditor can—and can’t—take if you default.

What happens when you can’t make mortgage payments?

Mortgage lenders usually offer a grace period on monthly payments. You typically have until the 15th of the month to make your payment without incurring any late fees or penalties. At this point, your lender will report your overdue payment to credit bureaus, and it will start to impact your credit score.

Is there a penalty for foreclosure on a loan?

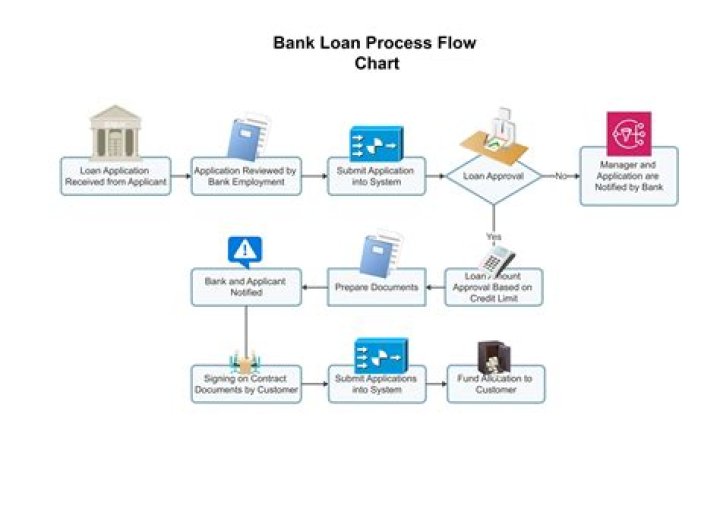

Some loans may have a penalty on foreclosure. Once the borrower has intimated the lender and the lender has accepted the proposal, the borrower must carry his/her ID Proof, cheque/ DD for foreclosure and loan account number. Along with that, the borrower must also request for the documents held by the NBFC/ Financial Institution. 2.

When to foreclose on property as a private lender?

In general, a foreclosure action can be initiated after the buyer/borrower has missed two to four consecutive monthly payments. Depending upon which state property is located, there may be one or two options to begin a foreclosure action: judicial foreclosure or non-judicial foreclosure (also known as a Power of Sale foreclosure).

Are there any downsides to a non judicial foreclosure?

The downside in non-judicial foreclosure is that land contract home sellers can’t sue their foreclosed homebuyers for negative loan balances. Non-judicial foreclosures, though, take less time than judicial foreclosures.

Can a bank foreclose a loan sooner than expected?

Sometimes, the borrower’s ability to repay a loan may increase over a period of time and they can foreclose the loan earlier than expected. Foreclosing a loan works perfectly for the borrower, however, the NBFC, Bank or Financial Institution involved may charge a penalty on prepaying the loan amount.